Popular narratives often attribute startup failures to flawed products, funding shortages, or market competition. Yet, for those observing closely, another quieter but equally potent factor emerges: legal fragility. A cap table entangled in informal promises, a co-founder threatening exit without vesting, a contract too onerous for customers to sign, intellectual property that legally belongs to freelancers, or compliance overlooked until flagged by regulators — each of these issues has derailed otherwise promising companies.

Recent experiences from across the ecosystem reveal how such risks, if unaddressed, erode credibility, but when properly managed, they become levers of growth.

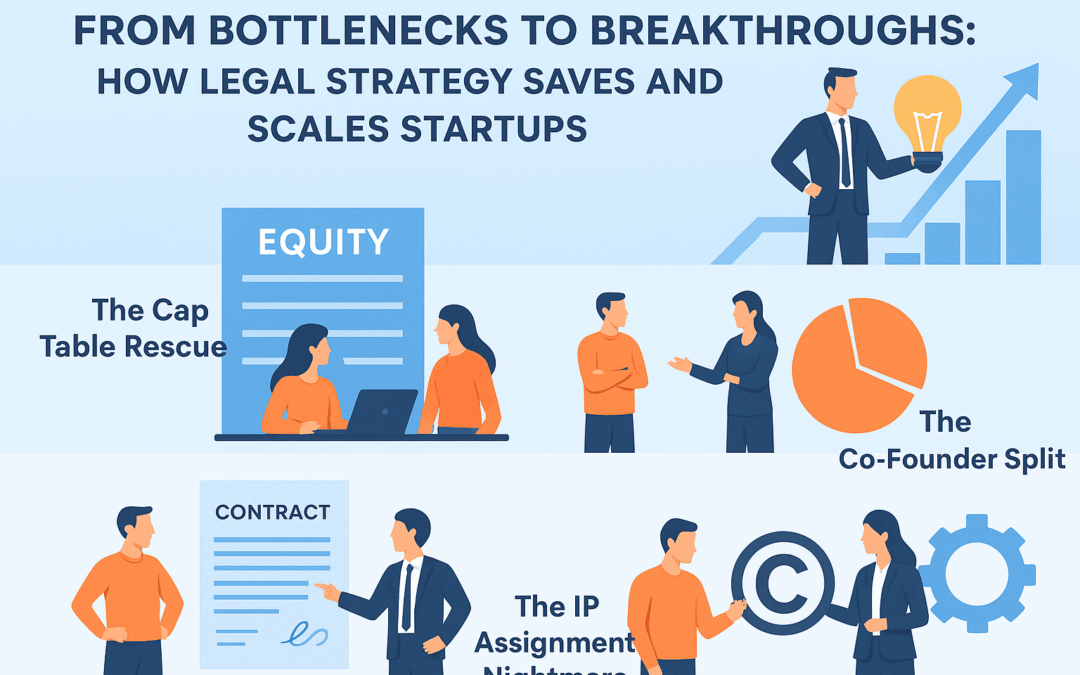

The Cap Table Rescue: Finance, Dilution, and ESOPs

A healthtech startup in Bangalore entered Series A negotiations with impressive metrics — ₹2 crore ARR and hospital partnerships. Yet, due diligence came to a standstill when investors discovered the cap table in disarray: informal promises of equity to advisors, unresolved share transfers, and the absence of an ESOP policy. What should have been a signal of maturity instead projected instability and poor governance.

Once the equity structure was regularised, an ESOP pool was carved out with a four-year vesting and one-year cliff, and dilution models were shared to assure the founder of future ownership stability; investor confidence returned. The clarity of ownership and forward planning transformed a red flag into reassurance, allowing negotiations to progress.

The Co-Founder Split: Negotiation, Mediation, and Reverse Vesting

An edtech company in Kolkata illustrates another common challenge. Two co-founders, aligned at inception, diverged sharply on growth strategy. With no founders’ agreement, no vesting schedule, and no buyback provision, one sought to exit with nearly half the equity within a year. Investors, concerned about governance risk, froze discussions.

A structured intervention — mediated settlement, reverse vesting of shares, incorporation of good leaver and bad leaver provisions, and a buyback option at fair value — stabilised the company. Investor hesitation dissipated once it became clear that founder continuity and equity alignment were secured. The absence of agreements had nearly destroyed value; their timely introduction restored it.

The Scary MSA: Contracts as Enablers or Barriers

Contracts, if drafted without business foresight, can repel rather than attract opportunity. A SaaS company in Gurgaon, despite strong technology, lost two enterprise deals in a single quarter. The obstacle was its Master Services Agreement — an imported template laden with unlimited liability clauses, vague service-level terms, and no mechanism for handling change requests. Procurement teams deemed it too risky to sign.

Revised documentation, condensed into a locally attuned three-page agreement, capped liability at a year’s fees, replaced refunds with credit mechanisms, and established a structured change request process. With these adjustments, clients found the contract workable, and deals that had stalled were swiftly concluded. In this instance, balanced drafting did not merely protect the company — it unlocked revenue and reassured investors about the company’s commercial maturity.

The IP Assignment Nightmare: Ownership on Paper

In Mumbai, a fintech startup preparing for funding encountered a fundamental question during diligence: Who owns the code? The answer was problematic. Early development had been outsourced without executing intellectual property assignment agreements. Legally, the freelancers retained ownership. What the company believed to be its core asset was not defensible on paper.

Through retrospective assignments, waivers of moral rights, proprietary information and inventions agreements for employees, and the replacement of open-source components carrying restrictive GPL obligations, ownership was secured. Only then did the funding process resume. This episode underscores a principle often overlooked by founders: unless intellectual property is expressly assigned, it does not belong to the company, regardless of who paid for its development.

The GDPR Roadblock: Compliance as Market Entry

A SaaS company in Kolkata, seeking European expansion, experienced repeated failures in late-stage sales. The reason was consistent: procurement officers declined to proceed once they realised the company had not implemented GDPR compliance. There were no Data Processing Agreements, no breach response protocol, and hosting arrangements failed EU cross-border data standards.

By instituting GDPR-compliant documentation, creating a CERT-In aligned breach response plan, and shifting data hosting to approved EU servers, the company overcame these barriers. Within three weeks, it closed its first European client, doubling recurring revenue and securing proof points for its Series A. Here, compliance functioned not as bureaucracy but as a prerequisite for market access.

The Common Thread: Legal Preparedness as Growth Capital

Across these scenarios, the thread is unmistakable. Cap tables, when disordered, repel investors; when disciplined, they instil confidence. Co-founder disagreements, if unmanaged, paralyse companies; if governed by structured agreements, they strengthen continuity. Contracts, if one-sided, lose business; if balanced, they accelerate sales. Intellectual property, if unassigned, undermines funding; if secured, it reassures investors. Compliance, if neglected, blocks expansion; if embedded early, it opens new geographies.

Final Word:

The legal framework of a startup is not peripheral administration. It is often the determinant of credibility, speed, and scalability. To treat law as a mere cost is to miss its role as growth capital in another form. Properly structured, it attracts investment, reassures clients, protects founders, and positions the company for sustainable expansion.

For today’s entrepreneurs, the imperative is clear: legal readiness is not an afterthought to growth. It is one of its essential conditions.